A major theme of analyses in this journal in recent years has been the erosion of the forces and institutions lending a degree of stability and coherence to global capitalism.1 This includes a widespread rejection of mainstream politicians and parties who, since the 1980s, tended to converge on a set of broadly neoliberal policies and conceptions, reshaping or building institutions to reinforce these. Neoliberalism is a slippery term, hard to pin down, often mutating and always heterogenous in its application. It was never a coherent system adopted wholesale across global capitalism. Nonetheless, there was at least a “family resemblance” between differing attempts to implement or impose it.2 Today, political forces associated with those policies tend to get punished at the polls.

That is certainly the case in Britain, where two parties outside the mainstream, the far-right Reform UK and the Green Party under its

left-wing leader Zack Polanski, dominated polling in May’s local elections. The projected national share of votes among the three traditional parties of British politics—Labour, the Liberal Democrats and the Conservatives—slipped to just 50 percent. A decade ago, the figure was 76 percent.3 Labour’s dismal results will likely trigger a battle for the leadership, expected to force the departure of Keir Starmer, who, just two years ago, led the party to a landslide victory.4 The fact that his most credible replacement, Andy Burnham, was standing in a by-election as this issue went to press, needing to return to parliament before any leadership challenge, speaks volumes about the inadequacy of the existing 402 Labour MPs.

Similar disruptions to mainstream politics are evident elsewhere. In the European Union, far-right parties lead the polls for key elections across the three most powerful countries: Germany, France and Italy. In the US, Donald Trump has reshaped the Republicans into a far-right MAGA party. Almost everywhere, liberal democracy has eroded since 2008, with a rise of authoritarian politics reversing the trend seen for most of the post-war period.5

If national political systems have become increasingly polarised and volatile, the same is true on an international scale, the terrain of inter-imperialist relations. Long-term shifts in economic power underpin these changes. In 1960, the US was responsible for 40 percent of global gross domestic product (GDP). By 1990, this had dropped to 26 percent. Through effective use of the dollar, still the dominant global currency, an initially extremely favourable global trade regime it helped to construct and a degree of reorganisation of its own industry, the US was able to prevent this figure dropping further over the subsequent three and a half decades. Moreover, the collapse of the Soviet Union and the Eastern Bloc enhanced the notion that the US would now reorganise the globe according to its precepts. Increasingly, though, a different picture has emerged. Aside from the US’s military blunders in Afghanistan and Iraq, a crucial element has been the economic rise of China—from 2 percent of global GDP in 1990 to around 17 percent, enough to credibly threaten US supremacy.6

The Iran conflict, the backdrop to a series of articles in this issue of International Socialism, gives expression to some of the consequences.7 The shifting imperial balance has spawned a growing number of sub-imperialisms able to contest power at a regional level. The region centred on the Middle East is cursed with a particularly large number—including Israel, Iran, the United Arab Emirates, Saudi Arabia and Turkey—all of which have played a role in recent conflicts, such as the dismemberment of Syria, the wars in Sudan and Yemen, and now the clash between Iran and the US and its allies. The changes to global imperialism are also reflected in the humble figure cut by Trump at his meeting with China’s leader Xi Jinping in Beijing in May 2026, following the US president’s failure to crush China economically through trade tariffs or Iran militarily through aerial bombardment.8

Trump’s Iran war shows how political instability interacts with two other interlinked dimensions of the new disorder. The first is ecological. There was a time when most leading politicians paid lip-service to issues such as global warming, even offering the odd policy to address the developing climate crisis. Those days are largely gone, just as ecological problems are beginning to factor in increasingly disruptive ways in the political economy of capitalism. For instance, as the left-wing economist James Meadway points out, the combination of the war in Iran and ecological factors—extreme weather conditions and a strengthening of the El Niño weather pattern—may strongly impact food prices in countries such as Britain this summer.9 As discussed below, even more immediate and deadly consequences are developing across parts of the Global South.

The second dimension is the economic. Capitalism is a global, interlinked economic, social and political system, with the functioning or malfunctioning of production, circulation and distribution lying at its base. The eruption of global economic crisis in 2008, followed in most advanced capitalist economies by bank bailouts and then austerity, helped accelerate the draining away of support from mainstream politics. However, none of the alternatives have succeeded in overcoming the underlying contradictions capitalism faces—indeed, new expressions of these contradictions have proliferated. In what follows, I will explore the vulnerabilities of capitalism to the kind of disruption triggered by the war in Iran.

Contours of contemporary capitalism

This journal has always been sceptical of glib talk of “globalisation” as a uniform process or one fundamentally transforming capitalism’s crisis-prone logic of exploitation and accumulation.10 There was, from 1945 through to 2008, an increasingly intensive and extensive pattern of internationalisation of capital, but this was always selective and uneven. Capital flows wherever it can most effectively generate profit. These processes are sensitive to labour costs but, if that were all there were to the picture, most manufacturing would simply relocate to sub-Saharan Africa. The location of capital also reflects access to markets; infrastructure and systems of social reproduction securing labour-power with the right qualities, often involving the state; supplies of raw materials and other networks of inputs; a sufficiently stable political environment; and so on. None of these things are static over time: capital and the state are constantly transforming their environs and reshaping where profits can most effectively be obtained. At the same time, the way capital becomes physically embedded in geographical locations and within broader networks of production can make it resistant to change.

Table 1: Where is capitalism concentrated?

|

Country/region or group |

% of world stock of public and private capital, 2019 |

% of world GDP, 2019 |

|

United States |

14.8% |

16.5% |

|

European Union |

15.9% |

15.9% |

|

China |

20.2% |

14.5% |

|

India |

6.0% |

7.4% |

|

Japan |

5.8% |

4.2% |

|

Russia |

3.1% |

3.3% |

|

Indonesia |

2.7% |

2.5% |

|

United Kingdom |

2.1% |

2.5% |

|

Brazil |

2.8% |

2.4% |

|

Mexico |

1.9% |

1.9% |

|

Turkey |

2.1% |

1.9% |

|

Korea |

2.0% |

1.8% |

|

Canada |

1.5% |

1.5% |

|

Saudi Arabia |

1.3% |

1.3% |

|

All other “advanced” economies (per country average) |

3.7% (0.3%) |

4.0% (0.3%) |

|

All other “emerging market” |

11.0% (0.1%) |

13.4% (0.2%) |

|

All other “low income developing” economies (per country average) |

3.0% (0.1%) |

5.0% (0.1%) |

Source: Calculated from the IMF Investment and Capital Stock Dataset (constant US dollar measures; latest available year used if 2019 data not available)

So, capital is expansive in its search for profits but also clusters in particular states and regions. The long-term results of these twin tendencies are shown in table 1. China is the big breakout centre of capital accumulation. The US, China and EU produce almost half of global GDP and contain just over half the total investment. A few other economies with huge populations—India, Indonesia, Brazil, Russia and Mexico make the top ten; Turkey, the top 20—represent a substantial mass of output and investment, but none competes with the big three on a per-capita basis. Among the major players, China and the US have been the most dynamic, with the EU lacking both the internal political cohesion and the market leaders in areas such as big tech to keep up. Germany, the EU’s industrial powerhouse, is stagnating amid rising energy costs and intensifying competition from Chinese exports.

The table is completed by other relatively large, advanced economies: Canada, Britain, Japan and South Korea, along with Saudi Arabia, historically an oil giant but one that has diversified into other industries. The low-income economies remain marginal from the perspective of global capital, despite this category including enormous countries such as Nigeria, Bangladesh or Vietnam. Even those categorised as “emerging market economies” by the IMF, when looked at individually, are a couple of orders of magnitude less powerful than the big players.

The rejigging of the global economy has significant implications.11 While Western leaders, flush with their triumph in the Cold War, might once have assumed that China’s 2001 entry into the World Trade Organization marked the advance of pax America—a neoliberal space united under the banners of the White House and Wall Street, the multinationals and the IMF—the outcome has been quite different. As noted above, there has been a sharpening of inter-imperialist tensions, playing out in economic, political and military conflicts. This, together with the growth of a power prepared to actively and openly use its state to drive and coordinate its economic ambitions, has contributed to a resurgence of state capitalism, with other states coming to mirror aspects of China’s approach to competition.12 As an advisor to the Washington-based Center for Strategic and International Studies commented on Trump’s visit to China: “The entire conversation about [trade] fairness is disappearing because…they think they wouldn’t get the Chinese to budge on these issues, but even more so because the US has decided that it will itself intervene heavily in the American economy”.13 Similar patterns are seen elsewhere. Germany, for instance, has embarked on a debt-financed drive to increase infrastructure and defence spending.

An additional factor also underpins the new state capitalism: the crucial role of the state in various forms of crisis-management.14 Far from the state disappearing with the shift to neoliberal policies, it continued to play an outsized role in economic life, even if its functions were restricted and redirected amid a veneration of market mechanisms. States, together with the central banks embedded in them, would play an important role in the bailout of the system in 2008-9, described by Marxist economist Andrew Kliman at the time as a “new manifestation of state capitalism…to save the capitalist system from itself”.15 By the time of the Covid-19 pandemic, Boris Johnson, an avowedly Thatcherite prime minister, was presiding over the largest peacetime state intervention seen by British capitalism, as the state stepped in to support the bulk of the labour market and protect businesses.16 High levels of state intervention, including debt-financed intervention, had by then been normalised,17 unsurprisingly leading to some on the left and within the working class asking why, if the state could rescue businesses teetering on the edge, it could not address their own multiple hardships and grievances.18

However, we are only seeing a partial return of state capitalism or, more accurately, a complex transition to a new situation that contains elements of state capitalism and elements of neoliberalism in an original synthesis.19 There are three reasons why capitalism cannot simply morph back to pre-neoliberal forms.

First, the ruling class retain deep-seated neoliberal sensibilities. Trump was perfectly happy to try to tear up decades of elite consensus around free trade through his tariff programme. Yet, he remains committed to a Reaganite programme of tax reductions for the rich and for businesses, along with the deregulation of banks and cryptocurrencies.20 He also shares with Bill Clinton and the New Democrats of the 1990s an antipathy towards publicly-funded welfare programmes.21 In Britain, part of the incoherence of Starmer’s Labour administration has been the inclusion of large numbers of unreconstructed Blairites, who, like the New Democrats, acted to consolidate a version of neoliberalism under New Labour.22 Attempts to “reform” welfare in a more neoliberal direction—sometimes successful, sometimes abortive—remain part of the political agenda in countries such as France and Germany.

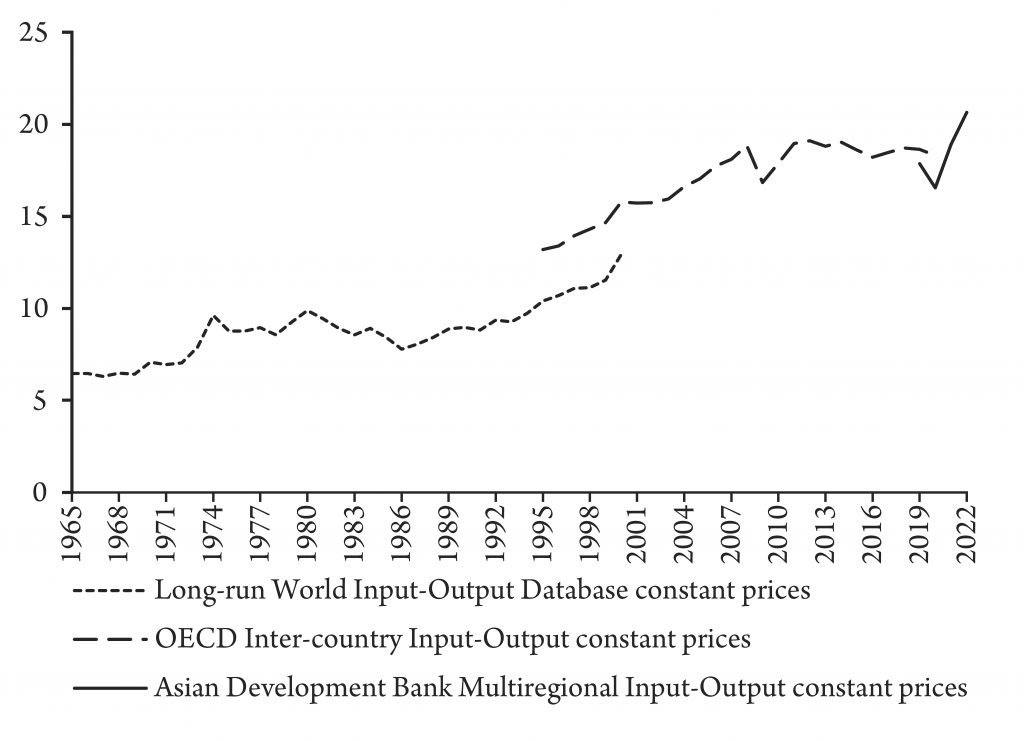

Second, the adoption of neoliberal policies supporting the liberalisation of trade and financial flows was not simply a response to the prolonged crisis of capitalism in the 1970s but also reflected the extent to which capital had

internationalised. As figure 1 suggests, the growth of trade has largely stalled since 2008. Yet, the overall rise in the value of trade, from 25 percent of GDP at the start of the 1970s to well over 50 percent today, has not been reversed. Previous periods of “deglobalisation”, such as that accompanying the breakdown of the international trade regime between 1914 and 1945, did see trade collapse—in that case from about 28 percent of GDP in the early 1910s to 13.4 percent in 1936.23 Compared to 1914, there is a greater distance for trade to fall, and we have not yet witnessed the outbreak of a world war or the equivalents of the collapse of the Gold Standard or eruption of a Great Depression. There is, though, some evidence that trade is becoming more concentrated across shorter “geopolitical distances”—in other words, that countries are refocusing their trade on countries with which they enjoy closer political relationships.24 The closure of the Strait of Hormuz has further highlighted the vulnerability of trade to “choke points” and will likely force further repatterning of trade and investment.

Figure 1: Global trade (sum of exports and imports) as a percentage of GDP

Source: OECD, 2025

However, none of this has stopped a veritable boom in trade in AI-related goods, which, in the case of the US, often means either continuing to import from China or substituting Chinese imports with those from other countries.25 Indeed, it has proven difficult for Trump to transform the global trade regime through his tariffs—and not just because his 10 percent global tariff was ruled to be illegal in the courts in May 2026. Market panics, along with Chinese retaliation, repeatedly caused Trump to retreat on aspects of his trade plans, leading the journalist Robert Armstrong to coin the acronym TACO: “Trump Always Chickens Out”.26 While the US could historically threaten to use its economic weight to isolate other economies, essentially weaponising globalisation, today this is not so simple. For instance, China has also begun using export controls to block supplies of rare earth minerals required by the tech industry to hit back at Trump and recently imposed restrictions on export to Japan of products with dual civilian and military applications.27

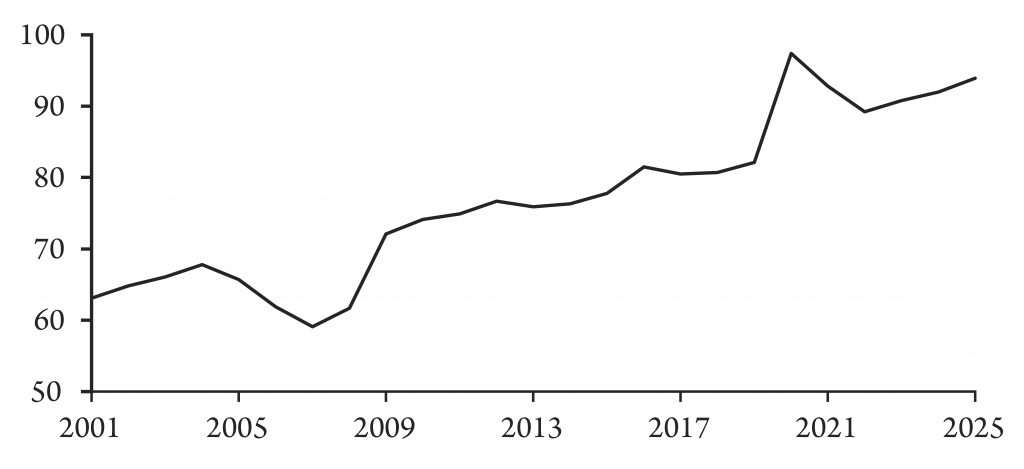

Figure 2: Global import-intensity of production (percentage)

Source: OECD, 2025

Trade conflicts do not just place at risk trade in finished goods but also the elaborate “capitalist value chains” underpinning recent forms of internationalisation of capital.28 Figure 2 shows import intensity: how much of the value of total output comes from intermediates imported to use in production. The rise is striking, showing how challenging it can be to reverse the internationalisation of capital, particularly given the scale of some of the giant enterprises involved in these networks. Amazon’s revenue is now equal to that of Austria’s; Apple’s, South Africa’s; Walmart’s, Argentina’s; Volkswagen’s, Pakistan’s; and Toyota’s, Portugal’s.29 Given the stakes, it is little surprise that Trump was accompanied on his recent visit to China by executives such as Jensen Huang of Nvidia, Tim Cook of Apple, Elon Musk of Tesla, Dian Powell McCormick of Meta or Kelly Ortberg of Boeing.30

A third reason why it is so hard to reverse elements inherited from the neoliberal era is the significance of global financial markets.31 As Costas Lapavitsas argues, productive capital “is tied to inflexible conditions of production”, whereas financial capital “organises liquidity, maturity transformation and credit under an institutional and legal infrastructure that gives it far greater elasticity”.32 The latter is essential to the operation of the former, particularly in developing and configuring capitalist value chains. Although banks remain important to the functioning of finance, since 2008-9, the central actors have been participants in the shadow banking system, such as hedge funds, private capital, insurance firms or money market funds.33 This shadow banking system, which stands outside the traditional framework of regulation imposed on banks, now holds just over half of global financial assets.34

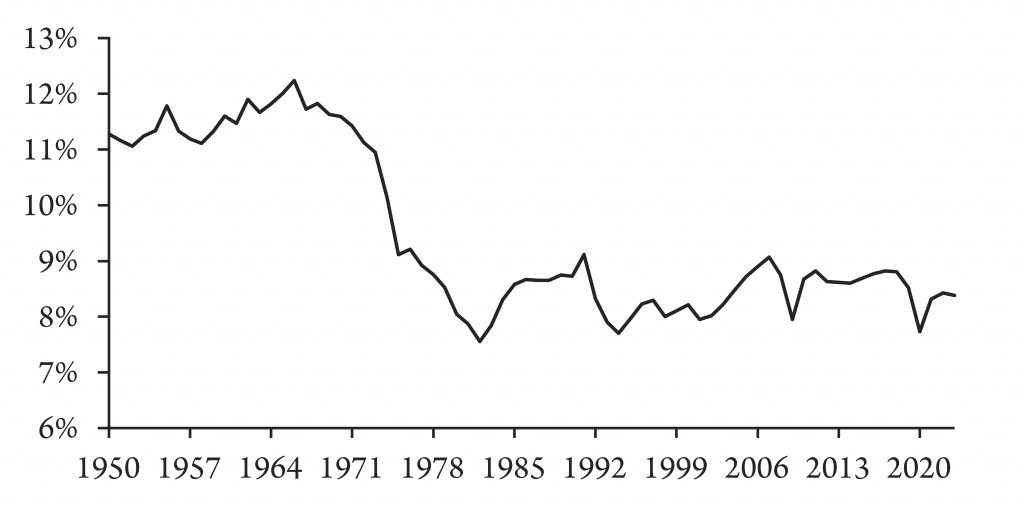

Figure 3: Global government gross debt as a percentage of GDP

Source: IMF World Economic Outlook, 2026

Finance, though, does not float free of states. As noted above, the role of the dollar, the closest approximation to what Karl Marx called “world money”, is one of the factors that has so far buttressed US imperialism.35 The dollar has, if anything, risen in significance as a means of settling international payments. Access to dollars remains crucial to the liquidity of financial systems of states that want to participate in the internationalisation of capital.36 US Treasury bonds and other dollar-denominated assets have declined a little as a share of global central bank reserves. However, no single currency has filled this gap. Indeed, the sharpest growth has been in gold—a traditional “safe-haven” in times of turmoil.37 Lapavitsas rightly argues that the absence of a “rival institutional complex with comparable reach”, has, despite the US’s economic and military limitations, created an “interregnum”, characterised by escalating conflict “on multiple fronts: trade, technology, finance, payments, reserves and military positioning”.38

There is also the issue of states’ dependence on creating public debt through bond markets. Government debt has grown significantly since the start of the millennium (figure 3), making states vulnerable to bond markets.39 This is particularly so in Britain, where government debt has risen from 30 percent of GDP in 2000 to 95 percent today, with a third of the debt held overseas. Admittedly, the Bank of England has made matters worse by flooding the market with bonds it had purchased as part of its quantitative easing programme in 2008-9 or during the pandemic.40 However, even where governments and central banks avoid poor policy choices, bond markets, in shaping the cost of borrowing, act as a powerful constraint on elected governments—unless they are prepared to challenge the logic of capitalism.41 Across the G7 economies, bond prices have fallen and bond yields trended up since the start of Trump’s war on Iran. Expectations of more government borrowing as inflation and other forms of economic disruption emanate from the war come at a time when markets in bonds are already relatively saturated.42

How strong is capitalism?

How strong and healthy is contemporary capitalism in the face of its current travails? While there are many possible metrics, Marxists often emphasise profit rates. This is not, as is sometimes claimed, because of a crude fixation on an immutable, continuous and inevitable decline of capitalism. Marx certainly never argued that profit rates always fall, and as the pandemic demonstrated, it is possible for the circulation of capital to break down for many reasons, without low profitability being the immediate trigger.

Nonetheless, the motive force of capitalism is the competitive accumulation of value that is pumped out of workers through exploitation. This means the potential pace of capital’s expansion—the ratio of new value created to the mass of capital already accumulated—is significant. Marx identified a tendency for profit rates to fall, alongside counteracting forces such as the cheapening of investments due to productivity growth or the intensification of exploitation. The resulting contradictions tend to work themselves out through crises, which devalue and destroy some of the mass of investment built up during expansionary phases, allowing the system to restore a level of profitability necessary to enter a new period of expansion. The financial system also facilitates both the expansion of capital and its destruction and devaluation in crisis.43

While there is a cyclical dimension to this pattern of boom and bust, I have argued that, over time, the secular dimension has become more important. The growth in size of the major firms, the enormous scale of the state in modern capitalism and the importance of finance, linking firms and states, makes the destruction of capital more perilous. Increasingly, states intervene to prevent a full-scale clear-out of the system.44 The result has been, in the traditionally most advanced centres of capital, a long period of subdued profitability and a developing tendency towards stagnation.

The measurement of profit rates is a complex question.45 Figure 4 offers a crude estimate using data from the Penn World Tables.46 Profit rates appear to fall precipitously as the long post-war boom comes to an end. Attacks on workers, a partial restructuring of the system through crisis, the opening of new areas of accumulation and the adoption of neoliberal measures combined to stop the fall, stabilising profit rates but at a level far lower than in the long boom.

Lower profit rates, together with the growing internationalisation of capital, help explain the growth of finance. If returns in the realm of production are limited, capitalists are likely to look to financial investments, including those of a speculative character, as a potential source of profit. The growth of finance in turn helps to sustain a mass of relatively unprofitable capital, which simply recycles its debts without engaging in much by way of investment. There is both a slackened pace of accumulation and an ever-expanding remit for credit to push capital beyond its limits and provide at least a veneer of dynamism. This has made capitalism fragile: each financial tremor spreads far and fast through the system, while small shifts in interest rates can suddenly make existing accumulations of debt seem unsustainable.

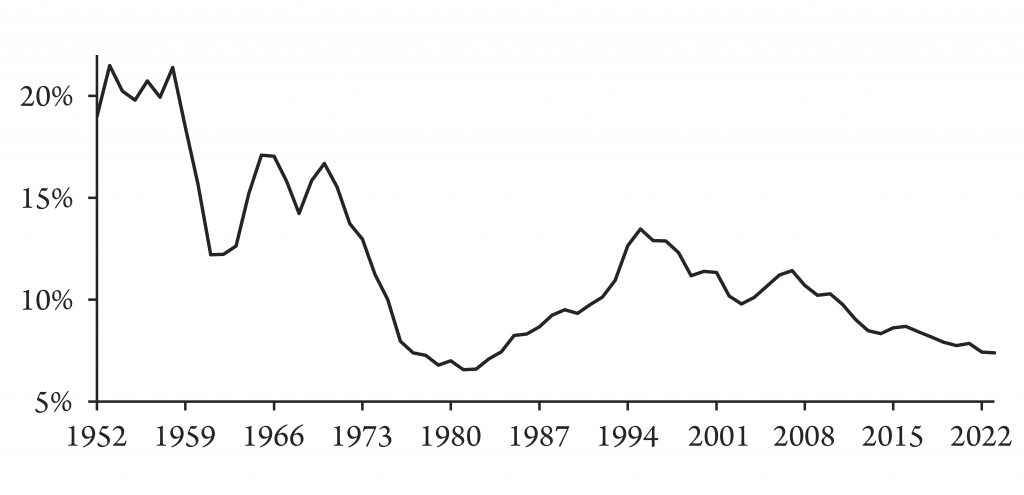

Figure 4: Estimates of global profit rates

Source: Calculated from PWT13.0

Figure 5: Estimates of Chinese profit rates

Source: Calculated from PWT13.0

The picture in China is a little different (figure 5). Its growing integration into global circuits of capital, first as an assembly platform for multinationals, later as a more independent centre of accumulation, saw profit rates rise well above the global average by the late 1990s. Yet, precisely as Marx would predict, the resulting extraordinarily rapid accumulation of capital has begun to choke off further accumulation. China is not only suffering some of the effects of the overaccumulation of capital; like the Western economies, it is also developing increasingly important markets in credit and finance to try to sustain its growth. Indeed, China’s debt-to-GDP ratio is now higher than that of the US, Britain or the Eurozone.47

Declining profitability does not preclude capitalists acquiring huge absolute profits. Nor does it mean that capitalism will collapse. However, it makes it vulnerable to disruptions such as those caused by the war in Iran. It should also give us pause when considering the hype around AI. The scale on which capital has been mobilised to develop and roll out the Large Language Models required by generative AI is colossal. The three big California-headquartered AI providers are OpenAI, Anthropic and Google, which, respectively, offer ChatGPT, Claude and Gemini. Table 2 shows how these firms, the infrastructures on which they rely, and the other tech giants intersect. There is an incestuous dynamic, even as these firms continue to compete with one another.48

Table 2: The ten largest firms by market capitalisation and their AI operations

|

Firm (ranked by market |

AI activities/investments |

|

Nvidia |

Develops chips used in AI. Investment of $30 billion in OpenAI (March 2026). Promised $10 billion investment in Anthropic (November 2025). Supplies Microsoft, Amazon, Google, Meta |

|

Alphabet (Google) |

Operates its own AI model, Gemini. One of the “big three” hyperscalers, providing colossal data centres required by tech firms. Its cloud facilities are also now used by both OpenAI and Anthropic. Committed to invest $40 billion in its rival, Anthropic (April 2026). |

|

Apple |

An outlier due to its limited investment in AI. But has entered a |

|

Microsoft |

Another of the “big three” hyperscalers. Major provider of cloud infrastructure for AI. Made an early investment in OpenAI, reaching $13 billion (2019-2025), and used ChatGPT to power its own Copilot AI assistant. Investment in OpenAI has now reached $135 billion. As of 2026, Microsoft is no longer the exclusive cloud-computing partner for OpenAI but remains its biggest partner. Microsoft also committed to a $5 billion investment in Anthropic and began hosting Anthropic’s models (2026). |

|

Amazon |

Another of the “big three” hyperscalers. Its cloud services are to be used on a massive scale by OpenAI and Anthropic. Currently Anthropic’s major partner for cloud services. Investment of $50 billion in OpenAI (March 2026). Committed to invest $25 billion in Anthropic (April 2026). |

|

TSMC |

Taiwanese company that manufactures most chips used in AI on behalf of firms such as Nvidia. Major customers for its chips |

|

Broadcom |

Develops chips used in AI. Supplies Google, Meta and Apple. |

|

Saudi Aramco |

The oil giant is one of only two non-tech firms on this list. However, it has partnered with Google to bring its cloud services to Saudi Arabia (2020). |

|

Tesla |

The other non-tech firm on this list, Elon Musk’s Tesla is focused on auto manufacturing, along with battery and solar panel development. Rumours swirl that it will be merged with Musk’s SpaceX, which includes the xAI division that has developed the underperforming Grok AI chatbot. Has an acrimonious relationship with OpenAI, of which Musk is listed as a founder, and which he once tried to absorb into Tesla. |

|

Meta |

Recently launched a new AI model of its own (April 2026) to compete with OpenAI, Anthropic and Google, and is building its own data centres to support this. Makes purchases from Nvidia. Relies on cloud services from Amazon, Google and Microsoft. |

Source: Company press releases and news reports

Because the table contains the companies with the biggest market capitalisation (prior to SpaceX's June IPO), it centres on firms caught up in the stock market exuberance over big tech. It leaves out the major Chinese competitors. These include Internet giants such as Baidu, Alibaba and Tencent, which are making their own substantial investments in AI, along with ByteDance, TikTok’s parent company, whose AI-powered chatbot has over 100 million daily users, and DeepSeek, the startup spun out of a hedge fund, whose R1 model, able to compete with those developed by far wealthier US firms, shocked the tech world in early 2025. Attempts by both the Trump administration and Joe Biden’s previous one to block China from accessing the most advanced chips and chip-making technologies reflect how AI is becoming a frontier for inter-imperialist rivalry. Beijing has responded by seeking to create its own AI chip fabrication infrastructure, based on Chinese firms such as Huawei, although without so far eroding the US’s technological lead.49

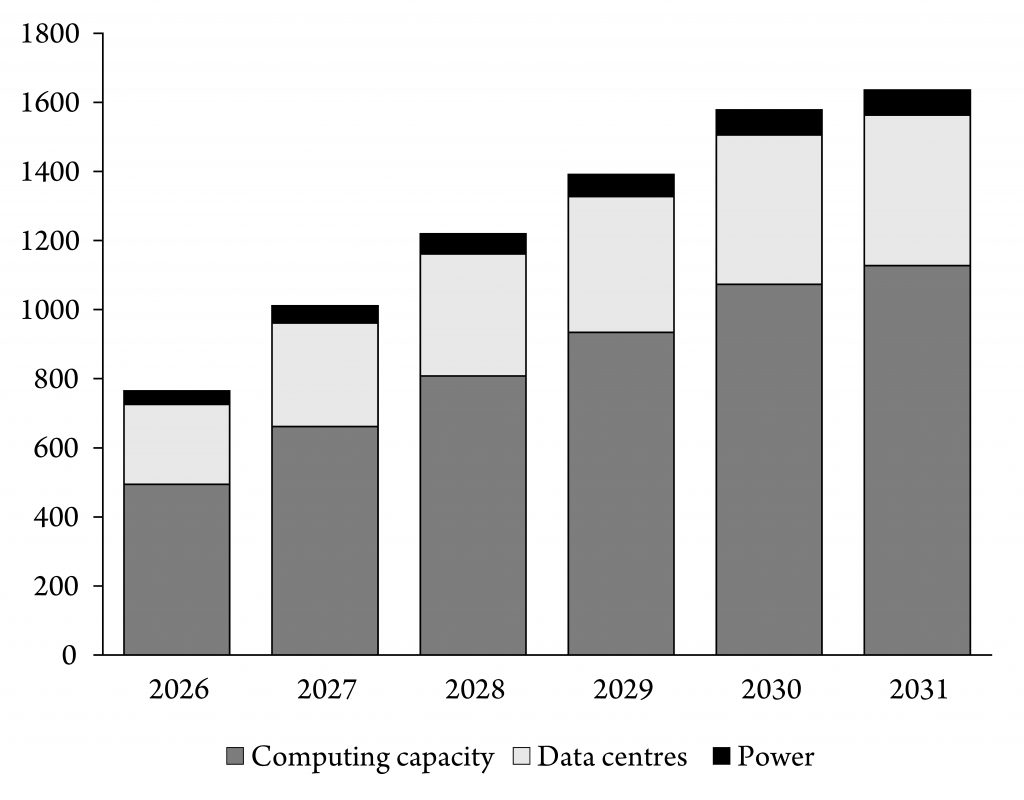

Figure 6: Projected AI-related capital expenditure (billions of US dollars)

Source: Lee and Greenbaum, 2026

The frenzy of investment in chips, data centres and energy infrastructure has become a major factor driving the economy and is a key reason why the US was able to ride out relatively unscathed the chaos engendered by Trump’s tariff plans. Figure 6 shows the projected investment by the major players in AI. To put this in context, non-financial businesses have recently undertaken around $4.5 trillion in annual capital expenditure. Adding over a trillion more would be a significant shift. The ethical dimension of building energy-guzzling, water-polluting data centres to drive a technology based on the plunder of humanity’s creative output simply to replace workers with glorified text autocomplete systems has been widely discussed. However, even from a narrow capitalist perspective, the investment appears unsustainable. Even commentators who attempt to justify the spending tend inadvertently to point to the profound systemic irrationality of capitalism:

Exuberance…need not imply irrationality… Whenever a radical new technology such as AI comes along, there is considerable uncertainty about its value… The biggest reason to call this a boom rather than a bubble…is the driving force behind it: a small group of established technology giants with coldly rational reasons to spend hundreds of billions on AI… The ChatGPT interface was an immediate and obvious threat to internet search (Alphabet: $3.8tn market cap). Algorithms, filtering and content creation with generative AI affect social media (Meta: $1.7tn). With a little imagination around AI agents and voice interfaces…the technology could also disrupt the smartphone (Apple: $4.05tn) and ecommerce (Amazon: $2.5tn) even before you get to Microsoft and the rest of the computing industry.

Protecting these enormously valuable businesses is easily worth spending a fortune just as an insurance policy, even if AI does not, in the end, create much new value… “If we end up misspending a couple of hundred billion dollars, I think that is going to be very unfortunate, obviously, but…I actually think the risk is higher on the other side,” [Meta founder Mark] Zuckerberg said in September.50

In the short term, firms such as Microsoft, Google and Amazon are confident that demand from other firms for their cloud computing facilities will continue to rise. However, the long-term problem is evident. As John Foley argues in an incisive piece for the Financial Times, it is not clear that AI will generate profits justifying the scale of investment. Indeed, the overall impact of the planned investments will be to reduce the amount of revenue received relative to the mass of fixed capital required to generate it. He notes that Apple, which has so far remained relatively aloof from the frenzy, makes over $8 for each dollar of fixed capital—compared to just $2 for Amazon. Meta, Google, Microsoft and Amazon each project further falls in this metric.51 An even more immediate risk is that disruption to supplies of inputs to chip fabrication, such as helium, due to conflicts such as the war on Iran, push up the cost of investments themselves, further undermining possible returns.

The big tech firms have historically had large amounts of their own cash to invest. The scale of investment they are now planning has seen forecasts for their free cashflow plummet, turning negative in the case of Amazon.52 Inevitably, they are therefore taking on increasing amounts of debt. In 2025 alone, the bonds issued by so-called hyperscalers reached $120 billion, 45 percent of the total issued by tech firms globally.53 This, though, understates the true amount of debt. Firms are also creating off balance-sheet Special Purpose Vehicles, separate entities created to fund specific activities such as operating a data centre, which attract investment from other companies, exposing them to risk if revenues are not as anticipated. This could currently amount to another $120 billion. If this sounds familiar, it should. Although not yet on the same scale, it is akin to the financial “innovation” that helped trigger the crash in the subprime mortgage market in the US in 2007-8.54 Some of the funding for these investments is also coming from private credit, an industry that has doubled in size from just over $1 trillion in 2020 to well in excess of $2 trillion today. Private credit itself has been a recent source of concerns, as turbulent markets have led to investors pulling out money at short notice.55

Other measures to raise the funds required by the tech giants for their investments include issuing new equity—Google issued $85 billion in shares earlier this year, with Meta likely to follow—and axing employees in other areas of their operations.56

A looming crisis?

As to whether the system will soon erupt in a 2008-9 style crisis, or worse, Marxism offers no definitive answers. All we can do is point to the fragility of the AI boom and the way it is deepening the contradictions of the system. Certainly, some sort of correction to the surge in share prices, centred on big tech, is widely expected.57 What is beyond doubt is that the war on Iran, and the resulting blockade of the Strait of Hormuz, has increased the strain on the global economy and made a crisis far more likely.

Oil tankers have barely moved through the Strait since late February 2026 and large parts of the oil infrastructure of the Gulf lie in ruins. Oil, urea, hydrogen and helium are among the commodities whose supply has been disrupted. At the time of writing, the impact had not yet been fully felt in the advanced economies, due to the drawing down of existing supplies and the release of strategic oil reserves by the International Energy Agency.58 In parts of the Global South, the initial effects had already become evident. Fuel costs have been a factor driving protests in Kenya as the government raised diesel prices by a quarter. Mozambique has seen minibus drivers, faced with 46 percent increases, strike.59 The disruption of fertiliser supplies will likely cause a longer-term food crisis across large numbers of African and Asian countries reliant on supplies from the Gulf.60

If the war continues or escalates, it will have a significant impact on the major economies of the Global North, with political ramifications. The rise in fuel prices has already put further pressure on Trump’s dismal approval ratings ahead of the mid-term elections scheduled for November.61 There is also a danger that our rulers make a bad situation worse. Under capitalism, shortages in essential commodities are dealt with through some combination of suppressing demand, choking off growth, and price rises, leading to inflation. At worst, as in the 1970s, an oil shock can trigger both at once, leading to stagflation.62 If inflation does rise sharply, a likely response from central banks will be to raise interest rates, following the standard neoliberal prescription to contain price rises. This is a blunt instrument, essentially discouraging spending and investment by making credit more expensive. Given that the global economy has increasingly come to rely on cheap credit, and hence low interest rates, this, too, can risk triggering a recession. Trump’s pick as chair of the US Federal Reserve, Kevin Warsh, who took up his role in May, will have to decide by the mid-June meeting of the Federal Open Market Committee whether to side with the president, who is known to favour efforts to cut interest rates.63

In this context, the left has two major challenges. The first is to continue to mobilise against the far right, which will seek to exploit any crisis, even one that far-right figures such as Trump and Benjamin Netanyahu play a role in creating. The second is to encourage workers and unions to move into battle over the developing cost-of-living crisis—and prepare for an even more devastating crisis if the current AI-driven boom turns to bust.64 Amid all this, there is a pressing need to explain the deeper irrationalities and contradictions of capitalism that have led us to this point, and to advocate for an internationalist and socialist alternative.

Joseph Choonara is the editor of International Socialism. He is the author of A Reader’s Guide to Marx’s Capital (Bookmarks, 2017) and Unravelling Capitalism: A Guide to Marxist Political Economy (2nd edition: Bookmarks, 2017).

Notes

1 Thanks to Rob Hoveman and Adrian Budd for feedback on earlier drafts.

2 Sperber, 2026, pp26-27.

3 BBC, 2026.

4 For more on British politics and the left, see Héctor Sierra’s article in this issue.

5 See the charts in Good God, Nord and Lindberg, 2026.

6 All data from the World Bank (current US dollars).

7 See the pieces by Anne Alexander, Simon Assaf and Phillip Marfleet in this issue.

8 Callinicos, 2026.

9 Meadway, 2026.

10 Harman, 1996; see also Harman, 2009, chapter 10.

11 In 1960, the contribution of a combination of the current EU countries, Japan, the US and Britain to global GDP and stocks of investment would have been about two-thirds of the total. Today these countries represent less than 40 percent.

12 Choonara, 2021a; Budd, 2026.

13 Lynch and Birnbaum, 2026.

14 Recent work by the IMF shows a striking increase in industrial policies from the time of the Covid-19 pandemic. There is a particularly big rise in policies related to national security and supply-chain resilience—Evenett and others, 2025, pp16-20.

15 Kliman, 2008, p63.

16 Choonara, 2021b.

17 Sperber, 2026, pp29-33, charts some of the shifts and their causes. However, he is over-reliant on identifying neoliberalism not simply as a set of policies, ideologies and institutions, but an “accumulation regime” (Sperber, 2026, pp35-38). This pushes the concept too far, demanding too much coherence of neoliberalism. It also means that Sperber (2026, p33) treats the economic failures eroding neoliberalism as “unforeseen shocks”, rather than rooting them in broader capitalist laws of motion.

18 Hence the importance of the debate on price controls, currently unfolding in several countries, including in Scotland, where the Scottish National Party leader John Swinney has suggested prices could be capped.

19 Sperber, 2026, p24, rightly points out that what we see today is “no longer obviously neoliberal” but equally not a reversion to Keynesianism or something similar. For an earlier analysis, see Choonara, 2025.

20 Husak, 2025.

21 See Daguerre, 2007, chapter 1.

22 Davidson, 2023, chapter 3. Lest we forget, Blair’s consolidation of neoliberalism was combined with a murderous alliance with the US neoconservatives of George W Bush’s administration, which rained bombs down on Afghanistan and Iraq before disastrously occupying them. Blair (2026) popped up after Labour’s miserable election results in May to advocate greater support for war on Iran and scrapping commitments to “net-zero”, as well as denouncing those “far left” (!) Labour politicians criticising neoliberalism or those he calls the “Radical Centre”.

23 Based on the estimates in Federico and Tena-Junguito, 2017. I have doubled their figures which are just for exports, rather than the sum of exports and imports. All estimates for this period should be treated with a pinch of salt.

24 See Seong and others, 2024.

25 Wolf, 2026a.

26 Armstong, 2025.

27 Keynes, 2026.

28 Benjamin Selwyn and Christin Bernhold (2025) use this phrase in place of the more traditional “global value chains” to emphasise the class relations underpinning them.

29 Selwyn and Bernhold, 2025, p3.

30 Hays and Mitchell, 2026.

31 Choonara, 2018, pp93-101.

32 Lapavitsas, 2026, p109.

33 Choonara, 2018, p97; Lapavitsas, 2026, pp117-118.

34 FSB, 2025.

35 Marx, 1990, pp240-244

36 Lapavitsas, 2026, pp126-133.

37 This reflects the rising price of gold as well as the rising volume of purchases by central banks—Storbeck and Hook, 2026.

38 Lapavitsas, 2026, p134.

39 Bonds are debt instruments, bought for a given price, which pay a fixed interest payment, known as the “coupon”, to investors. If the price of the bond falls, the ratio of the fixed interest to the price rises (and vice versa). This ratio, the “yield”, is effectively an interest rate, determining the rate at which issuers of bonds such as states borrow.

40 Selling off the bonds purchased during quantitative easing, rather than simply waiting for them to reach maturity, pushes down their prices—and hence pushes up yields. Daniela Gabor (2026) points out that without this British borrowing costs might be lower than the US’s. Moreover, she argues the Bank of England unnecessarily issued a large amount of inflation-linked bonds, while government policies have pushed pension funds, which together with insurance firms hold a fifth of bonds, to replace these with other investments to support defined contribution schemes.

41 Burnham is a case in point. Last year he famously warned that Britain was too much “in hock” to the bond markets. Now, in the context of a potential challenge for the Labour leadership, he has reassured capitalists that he supports the government’s current “fiscal rules” through which it seeks to restrict public debt.

42 Martin, 2026.

43 For further elaboration, see Marx, 1991, pp317-375; Harman, 2009, pp68-78; Callinicos, 2014, pp235-286; Choonara, 2017, pp64-77, 90-94.

44 Choonara, 2018, pp82-91.

45 For a recent discussion, see Karambakhsh, 2026.

46 I have used the internal rate of return for each economy where it is available, weighted with the capital stock. I do not claim this is the best way to perform these calculations, but the results are close to those of more sophisticated efforts. See, Roberts, 2026.

47 Williams, 2026. See also Pauls, 2021.

48 The continued competitive dimension is one reason why recent discussions of a new “technofeudalism” are so misleading—see Choonara, 2026.

49 McGuire, 2025. See Anne Alexander’s piece in this issue for more on how this plays out in the Middle East, which has sought to become a major hub for data centres.

50 Harding, 2025.

51 Foley, 2026.

52 See Foley, 2026.

53 OECD, 2026, chapter 2. It classifies as hyperscalers: Alphabet, Meta, Oracle, Amazon, IBM, Apple, Tencent, Alibaba and Microsoft.

54 Kinder, 2025. It is also reminiscent of the real estate collapse in China, from 2020 onwards, which showed how deeply intertwined the country’s housing had become with the shadow banking sector.

55 Private credit is part of a broader private capital industry. Although this is part of the shadow banking system, conventional banks also lend to the private credit industry—see Gara, Platt and Aliaj, 2026.

56 Morris, Fontanella-Khan and Murphy, 2026.

57 See, for instance, Parikh, 2026.

58 Wolf, 2026b.

59 Hook, Cotterill, Mark, Wallis and Pilling, 2026.

60 FAO, 2026.

61 In Britain, inflation fell in the year to April, largely due to government measures to hold down energy prices. A rise in the energy price cap in July will push inflation back up again.

62 Inflation is a complex phenomenon. It is often triggered by a shock to prices—such as the 1973 oil embargo or the Russian invasion of Ukraine in 2022—but it is sustained through an interaction between the creation of money by banks and central banks, and the production and sale of goods by firms. High levels of accumulation, at a time when profit rates are subdued, along with expansion of the money supply, tend to produce more sustained inflationary periods as firms take advantage of the injection of new money to raise prices and buttress their profits. One difference between today and 2022 is that the rise in inflation in the latter period came after a sharp expansion of the money supply as the pandemic hit. However, faced with a crisis, central banks are again likely to face a choice between expanding liquidity, and risking stagflation, or controlling it, and risking a deflationary collapse. For more on these issues, see Choonara, 2022, pp6-11.

63 The role of the bond market and the vast scale of US public debt mean that the US central bank does not unilaterally control interest rates.

64 See, for instance, Tengely-Evans, 2026.

References