A review of Capitalism in the 21st Century: Through the Prism of Value, Guglielmo Carchedi and Michael Roberts (Pluto, 2022), £19.99

Any new book by Guglielmo Carchedi and Michael Roberts is to be welcomed; both authors have had a long and fruitful engagement with Karl Marx’s economic theories. This new publication aims to explain some of the major issues in contemporary capitalism, using the framework of value theory and supported by empirical evidence. The book contains many insightful comments on value in relation to money, robots and knowledge as well as a clear explanation of crises that centres on the rate of profit. However, I find it necessary to challenge the authors’ view of the state in general, and its role in relation to imperialism and China in particular.1

From labour time to money

All books on value have the difficult task of trying to define what Marx meant by the term. In my view, Carchedi and Roberts are broadly correct in their approach, although I inevitably have some differences when it comes to the detail. Following Marx, they explain, “Commodities have two aspects—a use value and a value—because they are the products of both a specific (concrete) type of labour, which produces use values, and abstract labour, which produces value”.2 Value then takes the form of exchange value. Value and exchange value are distinct, although value can only express itself in terms of exchange value. The value of a commodity is seen as being the result of the exertion of human labour and is represented by a quantity of abstract labour time. This is the labour time socially necessary for the production of a commodity. Value then goes through a series of transformations that results in an exchange value, which itself is expressed in terms of money. So, money represents value, which in turn reflects labour time. Unfortunately, we cannot make simple statements like “money is labour time” for reasons I will touch upon later, but we can make statement such as “the value of a commodity is based on labour time” and “money represents a claim on part of the total labour time in society”.

Carchedi and Roberts argue that the transformation of abstract human labour into the value of commodities is the focus of Marx’s law of value and that three aspects of this law are crucial to explaining the developments in 21st century capitalism.3 These aspects are surplus value, the organic composition of capital and the rate of profit.

Regular readers of Roberts’s excellent blog, “The Next Recession”, will be familiar with many of the arguments presented here about money. Marx developed his theory of money in the first three chapters of the first volume of Capital:

Now, however, we have to perform a task never even attempted by bourgeois economics; we have to show the origin of the…dazzling money form… When this has been done, the mystery of money will immediately disappear.4

The logical development of the major categories that Marx develops in his analysis of money starts from labour time, moves through value and exchange value, and then ends up at money. He explains how money arises from what commodities have in common. They are all products of the expenditure of human labour time. This is the expenditure of abstract labour as it disregards the specific features of each type of labour. The socially necessary amount of this abstract labour required for production forms the magnitude of the value of a commodity. Yet, this value can only express itself in terms of exchange value, which itself is expressed in terms of money—the so-called universal equivalent.

Marx asks the following question to help clarify matters: “Why does not money directly represent labour-time, so that a piece of paper may represent, for example, x hours of labour?”5 He goes on to explain that, under capitalism, labour is indirectly social; it only becomes social through exchange. Labour time has to be transformed first into value and then into exchange value in order to be represented by money. Thus, money can only indirectly represent labour time. So, we can make statements such as that money represents a claim on part of the total labour time of society or money represents value, but it would be wrong to say money is labour time.6 The chief function of money is to measure this value. This is true for all money, including paper money, and irrespective of whether or not money is convertible to gold.

Carchedi and Roberts apply their analysis of money as a representation of value to new forms of payment that have emerged with the rise of the internet. In particular, they apply it to cryptocurrencies such as Bitcoin. The aim of Bitcoin is to bypass the transaction fees charged by the banks. Commerce on the internet relies on banks serving as a trusted third party between buyer and seller that processes electronic payments. Bitcoin allows any two willing parties to transact directly with one another without the need for a trusted third party. Cryptocurrencies are an electronic payment system that enable this using a transactional database or cryptographic ledger. This transactional database is based on blockchain technology, which “offers everyone the opportunity to participate in secure contracts over time, but without being able to avoid a record of what was agreed at that time”.7

Setting up a “wallet” so that one can conduct transactions in Bitcoin is still a difficult procedure, although there are specialist agencies that offer it as part of their services. However, since investors then have to pay intermediary fees rather than bank fees, this introduces a new third party and defeats one of the initial aims of Bitcoin. Moreover, so far, the real experience of Bitcoin is one of rife fraud, and it has quickly become a means of speculation and a vehicle for tax evasion as well as other criminal activities. Its chief importance for crime is keeping illegal transactions off credit card statements; crucially, in this regard, the owner of the money used to buy Bitcoins is allowed anonymity. There are also the environmental considerations of Bitcoin. The energy and other costs of Bitcoin are extremely high and vary from country to country. In Iceland, the mining of Bitcoin consumes nearly as much energy as the combined total for all of the country’s households.

So, is Bitcoin just a new means of speculation or is it a new form of money? The driver of Bitcoin and other cryptocurrencies has been the internet and online trade. Inasmuch as it functions as a means of payment, Bitcoin can be compared to money. It can represent value, but the speculative nature of cryptocurrencies impairs their function as a store of value and as a unit of account. Carchedi and Roberts conclude that Bitcoin can only be considered as an embryonic form of money: “At present, it functions only in an extremely limited way as money…but the adoption of digital currencies by central banks might change the role and nature of the Bitcoin”.8

Large companies could also try to introduce their own digital currencies to make payment for goods and services simpler and cheaper. Facebook planned to introduce “Libra” as its international currency before shelving the idea. Its aim was to provide goods and services with nearly zero transaction costs by bypassing international banks and national currencies. Libra would be a privatised currency, designed for commercial gain for Facebook and its investment backers. As Carchedi and Roberts argue, “With a successful Libra, there would be another new layer of credit-fuelled debt created, with repercussions for billions of people—and this time without any deposit insurance from governments!”9

The speed at which things are changing is remarkable. The Financial Times recently reported that physical money accounted for 60 per cent of transactions in Britain as recently as 2008, but now makes up only 15 per cent.10 States are responding by considering creating their own digital currencies, and there are already moves in the United States, China and Britain to explore the use of digital currencies. A digital dollar would, more than likely, drive out much of the competition.

Whatever form money takes, a major issue of concern is the return of inflation and the rise in the cost of living. Inflation, Carchedi and Roberts contend, is the result of the interplay of two factors: the combined purchasing power of wages and profits, and the quantity of money in circulation. They argue that, due to the labour-shedding nature of technological innovations, the share of constant capital (outlay on fixed assets, such as plant and machinery, and on raw materials) in total capital grows, leading to a rising organic composition of capital and the tendency of the rate of profit to fall. However, the rising share of constant capital in total capital also leads to the share of wages and profit in total capital falling. If inflation is determined by the combined pressure of wages and profits on prices, then the theory of inflation is tied to the theory of the tendency of the rate of profit to fall.

The authors argue that there has been a long-term decline in the US inflation rate measured by the Consumer Price Index from 1960 to 2019. Within that 60-year period, there are 2 phases. In the first, between 1960 and 1979, inflation was rising; in the second, between 1980 and 2019, inflation fell. The relationships between total value, constant capital, and the combined purchasing power of wages and profits are then used to explain the two different periods as well as the overall fall in the rate of inflation in the long run.

The theory has the merit of attempting to combine together the three areas, identified by Joseph Choonara, that should underly a theory of inflation. Choonara explains, “Broadly speaking, inflation depends on the interrelation between value creation through the expenditure of labour power, the creation of money (primarily through the credit system), and the relationship between capital accumulation and profit rates.”11

However, when it comes to empirically validating their theory with data, Carchedi and Roberts calculate a “value rate of inflation” by combining the purchasing power in value terms with money quantities. Yet, it is unclear why the combined purchasing power can be used to measure the amount of new value created. In my opinion, the work on inflation needs to be presented with much greater clarity and transparency. The view of Carchedi and Roberts is that neither mainstream nor Marxist theories of inflation have adequately explained changes in price inflation in economies with fiat currencies.12 Unfortunately, this still appears to be the case.13

Crises, robots and knowledge

Carchedi and Roberts are on firmer ground when discussing Marx’s theory of crisis. They offer strong theoretical and empirical evidence to place his law of the tendency of the rate of profit to fall at the centre of any explanation of recuring crises. The authors frame Marx’s “law” in terms of tendency and counter-tendencies:

As capitalism develops, new labour-saving and productivity-increasing technologies replace the old ones, and the amount of constant capital rises in relation to variable capital (outlay on wages). Because labour power hired with variable capital is the only part of capital that produces value (and thus also surplus value), the amount of value (and thus, other things being equal, of surplus value) falls relative to total capital invested. This depresses the rate of profit—unless there is a faster increase in the rate of surplus value, among other counter-tendencies. However, Marx contends that the law will assert itself sooner or later, that is, when the counter-tendencies can no longer counter the tendency.14

Marx’s law has a double edge. Even if the rate of profit falls, it is perfectly possible for the mass of profits to rise, and this can keep investment and production rising. Nonetheless, a persistently falling rate of profit will eventually slow and reverse the rise in the mass of profits. When the rate of profit falls to the point where the mass of profit goes into decline, this is a tipping point that opens the way for crisis. Profitability falls first, then investment falls. As profits go down, less is left for investments. Following an examination of the data, Carchedi and Roberts argue:

In every US recession since the war, it is broadly the same. The rate of profit falls before and during each recession by between 4 and 18 percent, and the mass of profit drops by between 6 and 26 percent (with the exception of the early 1990s recession).15

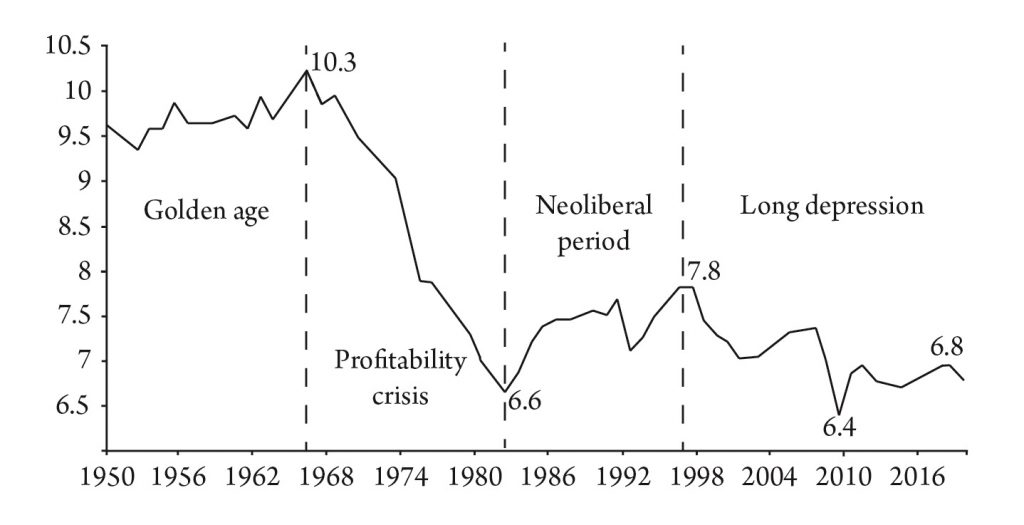

Counter-tendencies temporarily dampen or reverse the tendency of the rate of profit to fall. When they have exhausted their action, the tendency emerges once more. The operation of the counter-tendencies mean that crisis is temporary, and the accumulation process takes the form of periodic cycles. A crisis or a slump in production is necessary to correct and reverse the fall in the rate of profit and, eventually, any fall in the mass of profit. The graph below shows the changes in the rate of profit for the G20 countries between 1950 and 2019.

The cycle of boom and slump is explained in terms of changes in the rate of profit. A crisis is expressed in a fall in the average rate of profit, destruction of value, bankruptcy of the weakest capitals, reduced production and rising unemployment. In the slump the productive capitals that have survived are able to buy up means of production, raw materials and bankrupt companies at deflated prices. The recovery and boom express the opposite—following the destruction of value and a rise in the rate of profit, investment starts to pick up, creating rising profitability, expanded reproduction and growing employment. The course of each cycle is generated from within itself. According to Carchedi and Roberts, each crisis of capitalism has the same ultimate cause—falling profitability—but also has its own special features, including its own counter-tendencies. So, for example, the trigger for the 2007-9 Great Recession was the huge expansion of fictitious capital (mortgages and debt), but the underlying cause was the fall in the rate of profit:

The downward profitability cycle generates from within, first the crisis, and then the upward cycle. Accumulation and growth accelerate. However, the upswing, in its turn, generates from within itself the next downward profitability cycle.16

Carchedi and Roberts also critically examine alternative Marxist theories of crisis, namely, those focusing on instability and anarchy in the banking and financial sectors, underconsumption by the working class, and the inherent disproportion between different “departments” of the economy. Each of these theories has something to offer in understanding the complexities of a specific crisis, but none of them can explain recuring crises. The authors, I think convincingly, argue:

If crisis is recurrent and if they have different causes, these different causes can explain the different crises, but not their recurrence. If they are recurrent, they must have a common cause that manifests itself recurrently as different causes of different crises.17

They conclude that the law of the tendency of the rate of profit to fall “offers a causal explanation of the cyclical nature of capitalist accumulation, with an increasing body of empirical evidence to back it up. Nothing offered as an alternative is as compelling”.18

Figure 1: G20 rate of profit (percent)

Source: https://thenextrecession.wordpress.com/2020/09/20/more-on-a-world-rate-of-profit

As outlined by Carchedi and Roberts, Marx’s theory of crisis is both cyclical and secular (that is, long term). Although there is strong theoretical and empirical evidence to support the cyclical nature of crises and strong empirical evidence of the secular decline in the rate of profit, the theoretical arguments to explain this were unclear. Why is every new high point in profitability lower than the previous? Why are slumps failing to destroy enough value for the profit rate to be re-established at the same level as prior to the slump? No convincing explanation is offered, although it could be connected to the growing concentration and centralisation of capital, which results in companies that are just too big to be allowed to fail. The scale of the destruction of value required to restore the rate of profit to previous levels may well create more problems than it would solve.19

The expansion of robotic technology and artificial intelligence, Carchedi and Roberts claim, will also increase both the likelihood and magnitude of profitability crises:

It is very likely that slumps in capitalist production will intensify as machines increasingly replace labour. This is the great contradiction of capitalism—raising the productivity of labour through more machines reduces the profitability of capital.20

In value terms, replacing human labour by robots raises the productivity of the remaining workers and increases the profitability of those capitalists who are the first adopters. However, once the new robotic techniques have been generalised, the first adopters lose their advantage and profitability falls due to less workers being employed. This is one of Marx’s fundamental insights to the workings of capitalism; it is a contradiction that flows from the competitive accumulation of capital. So, in this sense, robots are just another stage in the growing productivity of labour and the consequent tendency of the rate of profit to fall.

Carchedi and Roberts argue that modern capitalism is increasingly no longer dominated by the production of things, but rather increasingly by the production of knowledge.21 The product of mental labour is knowledge, which has to be commodified and sold. Knowledge commodities can include commodified data, computer software, chemical formulae, recorded music, films and patented information. Both tangible objects and mental objects require the expenditure of human energy and can be productive of value:

The production of knowledge (mental labour) can be productive of value and surplus value if it is performed for capital… The computer programmer or website designer is in principle just as productive as the worker making the computer if both work for the computer company.22

The concept and design of a piece of software are produced by mental labour employed by capitalist companies. The companies exploit that labour and appropriate surplus value by selling or leasing the software. This is productive labour, and it produces value, even if knowledge is not a tangible object.

Imperialism is more than an economic phenomenon

Recurrent crises are one very important feature of 21st century capitalism; another is imperialism and the competition between states. As we have seen, competitive accumulation of capital leads to crises; however, it also leads to two other tendencies with particular significance for understanding the rise of capitalist imperialism. The first is the concentration and centralisation of capital within national economies; the second is the internationalisation and spread of capital outside the borders of the nation-state. These two tendencies have given rise to capitalist competition between states. Capitalist imperialism can thus be viewed as the coming together of two forms of capitalist competition: competition between states and competition between capitals. Imperialism is the fusion of economic and geopolitical competition. Out of this competition has arisen a global system of capitals and states competing for markets, investments and raw materials.

The unequal and combined nature of capitalist development results in unequal relations between nation-states and regions. A hierarchy of competing states has emerged. At the top are the more economically advanced states—for example, the US, China and Russia—which are the imperialist countries that compete with one another to form spheres of influence while dominating weaker states economically, militarily and politically. Lower down the hierarchy are less powerful states that compete over control of particular regions. In the Middle East, for example, these include Turkey, Israel and Iran. These smaller powers compete with each other, trying to form regional spheres of influence and domination.

Capitalist imperialism grows out of the accumulation of capital as the intersection of competition between capitalist states and capitalist firms. It is a global system of powerful states competing for domination of the world system using all the economic, military and political means at their disposal. Lenin, analysing capitalism at the start of the 20th century, explained the origins of the First World War as the outcome the conflict between rival imperialist powers.23

However, Carchedi and Roberts have a different view of imperialism to the one outlined above. In their view, imperialism is defined in terms of the relationship between a technologically advanced country and a technologically undeveloped one:24

We define imperialist exploitation as a persistent and long-term net appropriation of surplus value by the high-technology imperialist countries from the low-technology, dominated ones. This process is placed within the secular tendential fall in profitability, and not only in the imperialist countries, but also in the dominated ones.25

Within this definition, there is little sense of imperialism constituting a system or a stage in the development of capitalism, which are characterisations that would explain the inter-imperialist rivalry that led to the First World War and other major global conflicts. For Carchedi and Roberts, imperialism is a consequence of the formation of an international average rate of profit that transfers surplus value from the technologically underdeveloped countries to the technologically advanced countries.

Imperialist nation-states are defined as those with a persistently large number of high technology companies and a persistently higher national average organic composition of capital. This leads Carchedi and Roberts to define the imperialist countries as those making up the G7, which comprises Britain, Canada, France, Germany, Italy, Japan and the US. The dominated countries thus include the rest of the G20, which includes Brazil, China, India, Russia, Saudi Arabia, South Africa and Turkey.

According to the authors’ model, unequal exchange between the advanced and underdeveloped world arises because of the transfer of value associated with the formation of an international average rate of profit.26 However, the international appropriation of surplus value via the tendency towards a world rate of profit is just part of the normal working of the capitalist system. It is not specific to modern capitalism, even if the scope for the transfers of value has probably increased in contemporary capitalism.

Carchedi and Roberts also contend that rates of exploitation are higher in the dominated countries than in the imperialist countries. Initially, they argue that the higher the productivity, the lower the necessary labour time to produce commodities and, other things being equal, the higher the rate of surplus value. This would mean labour is more exploited in the imperialist countries. Yet, “To contain the loss of value, the dominated countries reduce wages, lengthen the working day and increase the intensity of labour; in short, they increase the rate of exploitation…above that of the imperialist countries…so that labour is more exploited in the dominated countries than in the imperialist countries”.27

This, however, may not be the case. In the imperialist countries, the potential to raise productivity and lower necessary labour time through technological change is almost limitless. Yet, the ability of the dominated countries to raise the rate of exploitation through reducing wages, lengthening the working day and increasing the intensity of work is limited by the basic survival needs of the working class. Whether or not this leads to the rate of exploitation being higher in the imperialist countries than the dominated countries is a matter for empirical investigation. With all of this we must remember that capitalist exploitation has a very specific definition—exploitation and poverty are not the same. Workers in underdeveloped countries may be simultaneously both poorer and less exploited than those in the economically advanced countries.

The authors’ economic theory of imperialism, based on the notion of unequal exchange, fails to account for the growing inter-imperialist rivalry in the 21st century between the US, China and Russia. It also fails to explain regional rivalries such as, for example, those in the Middle East involving Turkey, Iran, Saudi Arabia and Israel. Somewhat strikingly, their theory also ends up categorising China as a dominated country rather than as a rising imperialist power.

China is not in a “trapped transition” between capitalism and socialism

Carchedi and Roberts do see China as being in transition, but this is not a transition towards becoming a global superpower. Rather, it is a transition from capitalism to socialism. The term “transitional economy” is used to describe not just China, but also the economies of North Korea, Vietnam and Cuba.

Basing themselves on the work of the Soviet economist Evgeny Preobrazhensky, the authors list eight features of a transitional economy.28 They then compare the economies of Russia and China to this list, concluding that Russia between 1917 and 1989 and China from 1949 onwards should be considered transitional economies. The key conditions from this list satisfied by China are the loss of state power by capital, state ownership of the means of production and state planning of the economy. The authors accept that the law of value operates in a transitional economy, but they see this law as existing in competition with state planning: “A transitional economy is precisely where the law of value is in competition with the planning mechanism and collective production—the economy is in transition”.29

The association of planning, ownership and control by the state with a move towards socialism is very common across the entire political spectrum from left to right. Apparently, the greater state ownership and planning exists, the more progress towards socialism has been achieved. Nationalisation itself is seen as progressive. This is a conception of socialism that has been rejected by the political tradition associated with this journal, which has always argued that a transition towards a socialist society requires direct workers’ control over the economy.

Of course, challenging the idea that nationalisation and socialism are synonymous does not rule out that it might be appropriate to demand that the capitalist state nationalise an industry in some circumstances. The state is in a position to transfer value from profitable companies to unprofitable ones via the tax system, and this can be a practical reform worth advocating, for example, in order to protect jobs. That said, we need to be clear about why such a demand should be seen as a reform of capitalism rather than part of a move towards socialism.

First, the idea that state ownership does away with the capitalist nature of the productive forces is false. Were it true, large parts of the Global North would already count as non-capitalist, since big sections of the workforce in many such countries are employed by the state. Indeed, Carchedi and Roberts appear to partially agree with this point. Writing about China, they argue:

In the state sector, workers generate surplus labour, and a bureaucratic elite control that surplus. In this sense, the state sector is capitalist in character. Workers are exploited, and the law of value operates here. Yet, the state sector produces goods and services primarily according to planning targets and not for individual profit. So, in this sense, they are not capitalist as state enterprises are in capitalist countries.30

Second, although Carchedi and Roberts regard the issue of planning and the law of value as opposites that are in competition with one another, planning actually takes place in the context of competition rather than in opposition to it. Indeed, capitalism simply could not exist without large-scale planning, which they acknowledge:

Already, today, in the most advanced capitalist countries, the bulk of both consumer and producer goods are not produced in any sense as a response to “market signals”… The bulk of current production corresponds to established consumption patterns and predetermined production techniques that are largely, if not completely, independent of the market.31

The issue is thus not planning as such. The totalising logic of capital means that planning is shaped and determined by capitalist imperatives. The issue is whether the contents of the plan are determined by the producers themselves and not by economic laws over which those producers have no control. If a company, whether private or state owned, is to compete effectively in the context of a world market governed by the law of value, planning must ultimately be governed by economic laws and imperatives over which the firm has no control. Planning in a capitalist society cannot escape the law of value. Thus, the absence of competitive markets does not mean that the law of value ceases to operate. Instead, it means the law of value has changed its form and modified the way in which it operates. The law of value is not limited to market determination. There is more on this below.

Third, the concept of a transition deployed by Carchedi and Roberts equates capitalism with a specific form of ownership, and a transitional economy with a different form of ownership, but forms of ownership are merely legal relations. The replacement of private ownership with state ownership is a legal act. Ownership of the means of production can go from private hands to the state and back again without affecting the capitalist nature of the system.

In the view of Carchedi and Roberts, transitional economies are a description of economies that are now in an intermediate stage between capitalism and socialism. They argue, however, that China is not moving towards socialism, but rather is in a “trapped transition”. This raises all sorts of questions. For Marx, the existence of a state is evidence for the domination of one class over another. If the Chinese state owns the bulk of the means of production, what class is in power in China? What is the nature of this state? What is the mode of production? The whole idea of a transitional economy outside a period of revolutionary transformation appears to make little sense within the context of Marx’s thought.

There is, of course, a place for the concept of a transitional economy in a period of revolutionary transformation. Between capitalism and communism lies a period of revolutionary transformation from one into the other. A transitional economy could come into existence after the first successful socialist revolution and continue while this revolution spread internationally until it reached a critical mass and the restoration of capitalism was no longer a threat. Spreading the revolution globally would be decisive. Failure to internationalise would leave the revolution isolated, embedded in the global capitalist economy and locked into a competitive battle with capitals elsewhere in the world. Capital’s totalising logic would reassert itself.

The necessity of the capitalist state

The classical manifestation of capitalism as free market competitive capitalism only really exists in the textbooks. The operation of the law of value and the accumulation of capital has historically resulted in the units of capital becoming larger and larger. What Marx called the concentration and centralisation of capital has led to monopolies and multinational corporations as well as state capitalisms, in which single capitals appear in the form of a nation-state, with the state owning the means of production.32 The state is not neutral, and state ownership of the means of production refers to ownership by a capitalist state. None of these different forms of appearance of capital have changed the essence of capitalist social relations, but they have modified the way in which the law of value operates.

Capitalism is a society in which the law of value operates. However, if we imagine the law of value as operating exclusively through market mechanisms and without modifications in different historical and national contexts, then we can no longer really see capitalism existing anywhere. What we have at best is mixed economies, part private, part state. In his path-breaking State Capitalism in Russia, Tony Cliff argued that state capitalism represents a partial negation of the law of value.33 Yet, this partial negation only takes place on the basis of the law of value continuing to operate at the level of the global economy.34

It is very common to associate the law of value with market determination. However, the law of value is not about how individual market prices are formed; rather, it concerns the regulation of competition between capitals through the formation of socially necessary labour time. Marx argued that, when the law of value is operative, “the labour time necessary to produce the products asserts itself as a regulative law of nature. In the same way, the law of gravity asserts itself when a person’s house collapses on top of him.”35

An economic law can have more than one form of manifestation. The law of gravity can manifest itself as a house falling down or as the rising and falling of the tides—both are manifestations of the same law. Likewise, the law of value can manifest itself through competitive markets or, in their absence, through other forms of competition. In the case of the Soviet Union, the form of competition was predominantly military. What is common is the underlying determination of changes in productivity and socially necessary labour time by competition between different capitals. The regulation occurs behind the backs of both private and state capitals. In one case, market competition compels capitalists to raise the level of productivity by reducing socially necessary labour time; in the other case, military competition plays the same role, compelling state capitalists to raise the level of productivity and reduce socially necessary labour time. The competitive accumulation of state capital is based on the exploitation of wage labour, with competition in the market replaced by competition between states.

Carchedi and Roberts do argue that “the law of value operates in the Chinese economy”. Yet, according to them, “The impact is distorted, curbed and blocked by bureaucratic interference from the state and the party structure to the point that capitalists cannot yet fully dominate and direct the trajectory of the Chinese economy”.36 The problem with this analysis is that it underestimates the totalising effect of capitalist social relations. In both forms of capitalism—private and state—there is the production of commodities: things that can be bought and sold for pounds, dollars, rubles and yuans. However, there are modifications to the way the law of value operates within a state capitalist society. Money exists as the universal equivalent and represents a claim on the total labour time of society. Labour power exists as a commodity and is exchanged between the worker and the state; in exchange for the sale of their labour power, workers receive a wage that does not represent the full value of their work. Workers produce surplus value, and this is accumulated by the state. The process of forming a general rate of profit through the formation of prices of production is largely absent, and the law of value is partially negated within the state as a result of this. The state effectively seals the surplus value produced within its boundaries and prevents it from being accessed by other capitals, whether state or private. Competition with other states forces the state to continually increase the accumulation of state capital by raising the level of productivity and increasing the level of exploitation.37

The notion of the state acting as capital is essential to understanding capitalism in the 21st century. China, the second largest economy in the world, has a large state sector; Aramco, the largest oil and gas producing company in the world, is owned by the Saudi Arabian state; a number of countries, such as Cuba and Vietnam, are state-run economies; and many other economies are a mixture of private and state capital. All exist within a ruthlessly competitive global capitalist system. In times of crisis, ruling classes often turn to state intervention to limit economic damage, as happened on a global scale in response to the world financial crisis in 2007-9 and the Covid-19 pandemic in 2020. In my view, state capitalism is not only an essential analytical concept for contemporary capitalism; it also provides a political orientation in relation to the state. It points towards the necessity for a revolutionary overthrow of these societies, as envisioned by Marx.

The path to transforming society will benefit enormously from having a clear understanding of how capitalism in the 21st century works. Capitalism is always evolving, and many of today’s analysists of capitalism have left the theory of value behind. This book, however, swims against that stream. It is a significant contribution to the important project of understanding contemporary capitalism using the framework of value theory with the support of empirical evidence.

Nick Moore is a long-standing member of the SWP in North London and taught mathematics at a sixth form college.

Notes

1 Thanks to Joseph Choonara and Pete Green for comments on an earlier draft.

2 As well as this, they also write on the first page of the book, “Commodities then have value with dual aspects.” In my view, this is at best confusing. Commodities have a dual aspect: use value and value. This statement concerning value having a dual aspect is repeated on pages 156 and 187.

3 This is a very broad definition of the law of value. I prefer a narrower definition that focuses on socially necessary labour time and its role in the regulation of competition between capitals. From this perspective, surplus value, the organic composition of capital and the rate of profit are seen as part of a more general theory of value.

4 Marx, 1976, p139.

5 Marx, 1976, p188.

6 The connection between money and labour time is still completely foreign to mainstream economic theory. Unfortunately, some Marxists make the mistake of either severing value from labour time, as measured by clock time, or alternatively collapsing value into exchange value.

7 Carchedi and Roberts, 2023, pp65-66.

8 Carchedi and Roberts, 2023, p69.

9 Carchedi and Roberts, 2023, p75.

10 Giles and Venkataramakrishnan, 2023.

11 Choonara, 2022a, p12; Choonara, 2022b, pp6-11.

12 In mainstream economics, inflation is explained as a result of a “cost push” mechanism, as a consequence of a “demand pull” mechanism or as the outcome of changes in the money supply. Fiat money is paper money that cannot be converted into gold.

13 I understand that Carchedi and Roberts are themselves unhappy with elements of their treatment of inflation here, and they are working on a new paper addressing these issues.

14 Carchedi and Roberts, 2023, p97.

15 Carchedi and Roberts, 2023, p96.

16 Carchedi and Roberts, 2023, p98.

17 Carchedi and Roberts, 2023, p116.

18 Carchedi and Roberts, 2023, p116.

19 For more on this, see Choonara, 2018.

20 Carchedi and Roberts, 2023, p156.

21 Carchedi and Roberts argue that knowledge is “material”. This, to my mind, is too reductionist. An alternative theory would see knowledge as being determined by material reality but not reducible to it. Such a theory would involve concepts such as emergence and irreducibility.

22 Carchedi and Roberts, 2023, p163.

23 This understanding of imperialism is based on Callinicos, 1991 and 2009.

24 Carchedi and Roberts do acknowledge that they are only dealing with the economic side of imperialism. Yet, they then proceed to classify countries as imperialist or non-imperialist based on this narrow economic definition.

25 Carchedi and Roberts, 2023, p117.

26 For a discussion of theories of unequal exchange, see Harris, 1986. The world average rate of profit is calculated by assuming there emerges only one average rate of profit in each country. There is then an international equalisation of the national rates of profit. However, the world economy is not divided into blocks of national capital, and it would thus be more appropriate to average sectors or branches of global production.

27 Carchedi and Roberts, 2023, p136.

28 See Preobrazhensky, 1965.

29 Carchedi and Roberts, 2023, p218.

30 Carchedi and Roberts, 2023, p224.

31 Carchedi and Roberts, 2023, p227.

32 Historically, the creation of state capitalist systems has not been confined to the Soviet Union and China, but has often been the result of revolutionary nationalist forces coming to power in formerly colonised countries. These include the 26 July Movement, led by Fidel Castro, who only declared himself a Marxist in 1961, two years after the Cuban Revolution had brought him to power, after developing diplomatic relations with the Soviet Union.

33 The first draft of State Capitalism in Russia appeared in 1948.

34 Cliff, 1988, p173.

35 Marx, 1976, p168.

36 Carchedi and Roberts, 2023, p215

37 For more analysis of the modifications to the law of value in the Soviet Union, see an unpublished article I wrote in 1990, entitled “Marx’s Theory of Value and State Capitalism”, which is available from me via the editors of International Socialism.

References